Earning more or building up assets over time can change how your finances are managed, but many people are unsure when they cross into what’s considered “high net worth.” It’s not always obvious, and the definition can vary depending on the context.

In the UK, certain thresholds are used by tax authorities and financial institutions to identify individuals with more complex financial situations. These thresholds are not just about income, but also include savings, investments, and property.

Knowing whether you fall into the “high net worth” category matters as it can affect how your tax affairs are handled, the level of reporting required, and the kind of financial advice you may need.

Keep reading to find out how high net worth status is defined in the UK and what it could mean for your finances.

What is a High Net Worth Individual?

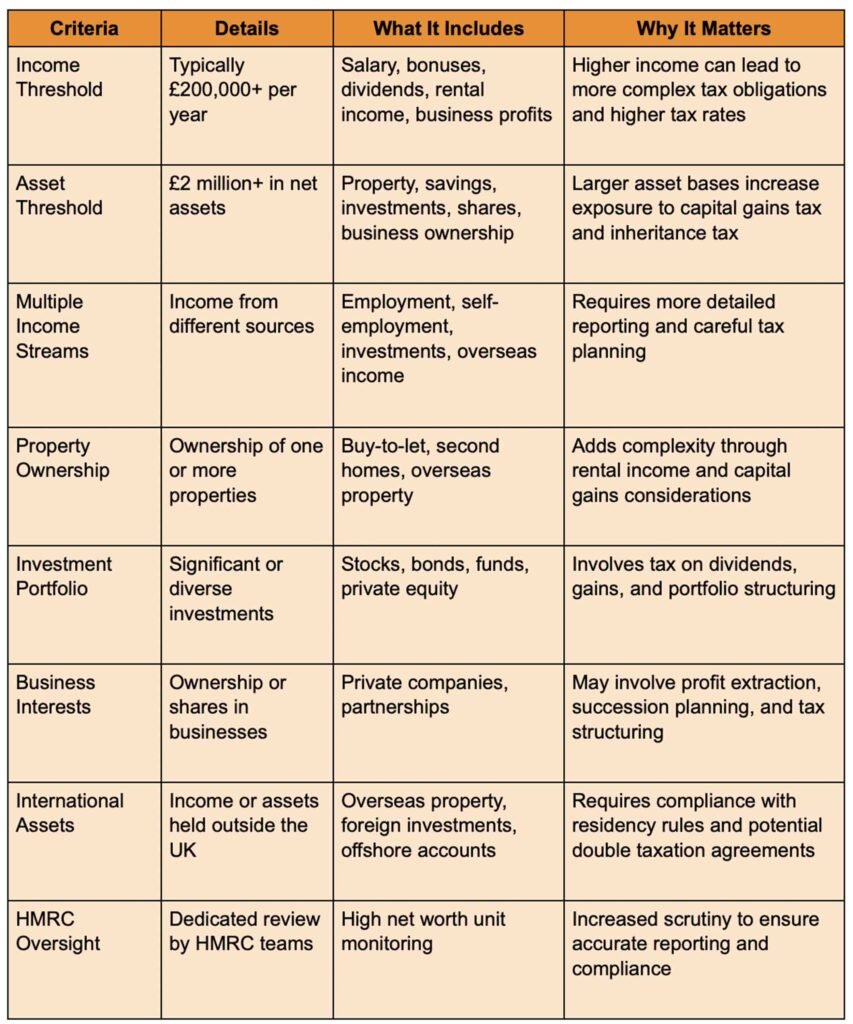

In the UK, a high net worth individual (HNWI) is typically defined using financial thresholds that reflect both income and overall wealth. These definitions are often used by HM Revenue and Customs to identify individuals whose financial affairs may be more complex.

In general terms, you may fall into this category if your annual income reaches around £200,000 or more, or if your net assets are valued at £2 million or above. Net assets usually include property, savings, and investments, while everyday personal items are not typically counted unless they hold investment value.

Knowing whether you fall into this category is important because it can influence how your finances are managed. High net worth individuals are more likely to face complex tax situations, stricter reporting expectations, and a greater need for structured financial planning. Recognising your position early can help you stay organised, make informed decisions, and avoid potential issues as your wealth grows.

How Is High Net Worth Status Classified in the UK?

High net worth status in the UK is based on a mix of income, assets, and the overall complexity of an individual’s financial position. While there is no single public register, HM Revenue and Customs uses specific criteria to identify individuals who may require closer attention due to the scale or structure of their finances.

This classification helps determine the level of oversight, reporting expectations, and the type of support that may be needed to manage tax affairs properly.

How Are High Net Worth Individuals Taxed in the UK?

High net worth individuals follow the same tax framework as other UK taxpayers, but their financial structure often involves more layers. Multiple income sources, asset disposals, and long-term wealth planning all come into play, which can make taxation more complex. It’s not always easy to keep track of how different taxes apply, especially when finances grow over time.

This is where working with experienced accountants for high-net-worth individuals like Haggards Crowther can help, especially when managing obligations, structuring finances, and staying compliant with HMRC requirements.

Here are the key taxes that often require closer attention:

Income Tax

Income tax remains the foundation of personal taxation. In the UK, earnings are split across bands, with the additional rate of 45% applying to income above £125,140. One key detail for high earners is the gradual loss of the personal allowance once income exceeds £100,000. For every £2 earned above this threshold, £1 of the allowance is reduced, which can create an effective tax rate of up to 60% within that band.

Income may also come from different sources, including salary, bonuses, rental income, and business profits. Each source needs to be reported correctly, and timing can affect how much tax is due within a given year.

Capital Gains Tax (CGT)

Capital gains tax applies when assets are sold at a profit. This commonly includes shares, investment portfolios, and additional properties. For higher-rate taxpayers, CGT is typically charged at 20% on most assets, while residential property gains can be taxed at 24%.

There is an annual exemption (currently £3,000), but gains above this are taxable. For high-net-worth individuals, frequent buying and selling of assets can quickly lead to larger CGT liabilities. Planning the timing of disposals, using allowances efficiently, and considering transfers between spouses are often used to manage exposure.

Dividend Tax

Dividend income is common for those with investments or company ownership. After the dividend allowance (currently £500), income is taxed at different rates depending on your tax band. For additional rate taxpayers, this can reach over 39%.

Although dividend tax rates are lower than standard income tax, they still add up, especially when dividends form a large portion of income. Structuring how profits are taken from a business or investment portfolio becomes an important part of tax planning.

Inheritance Tax (IHT)

Inheritance tax becomes more relevant as wealth grows. The standard nil-rate band is £325,000, with an additional residence nil-rate band available in certain cases. Anything above these thresholds may be taxed at 40%.

For high-net-worth individuals, estates often include property, investments, and business interests, which can push total value well above the threshold. Planning strategies may include gifting, trusts, or structuring assets in a way that reduces future liabilities.

International Tax Considerations

For those with overseas income, assets, or business interests, tax becomes more complex. Residency status determines how worldwide income is taxed in the UK, while domicile status can affect access to certain tax treatments.

Double taxation agreements exist between the UK and other countries to prevent income from being taxed twice, but navigating these rules can still be challenging. Reporting requirements are also stricter when foreign income or assets are involved.

Currency movements, overseas property ownership, and cross-border investments can all influence tax exposure, making accurate reporting and planning essential.

Know Your Financial Position

Understanding whether you qualify as a high net worth individual gives you a clearer view of your financial position and what comes with it. It’s not just about hitting a certain number. It’s about recognising when your finances start to require more careful planning and attention.

As income and assets grow, so do the responsibilities around managing tax, investments, and long-term goals. Taking the time to review your situation can help you stay organised and avoid unnecessary complications later on. It also puts you in a better position to make informed decisions that support your future.

Having the right support in place can make a real difference. With a clear understanding of your status and obligations, you can manage your wealth more confidently and keep everything on track.